The historically low cash rate has left investors with a difficult choice – remain in cash earning nominal returns, or look for higher yielding, and invariably higher risk investments.

Investors have inevitably chosen the latter, and as the appetite for yield across the fixed income spectrum has become insatiable, one asset class is generally overlooked – structured credit.

The Big Short

Investors have largely shied away from structured credit, created via securitisation, with the memories of the 2008 US subprime mortgage crisis persisting. In popular culture, this is portrayed in Adam McKay’s movie adaptation of Michael Lewis' novel, The Big Short.

Here we saw securitisation at its worst – borrowers with no income or assets obtaining mortgages, investment banks re-securitising pools of poor performing loans and ratings agencies exploiting a conflicted fee model. The result: unprecedented losses in US residential mortgage-backed securities (RMBS) during the housing downturn.

Misconceptions overshadow true value

The emotional response to this asset class, coupled with its perceived complexity has overshadowed its true value in providing investors with higher risk-adjusted yields compared with other credit products.

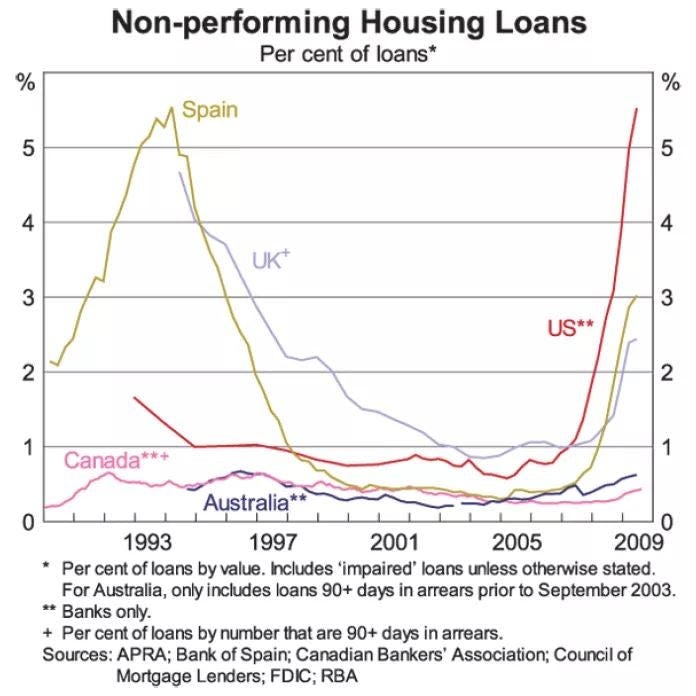

Further and specific to the local market, unlike in the US, Australian mortgages performed well during the global financial crisis (GFC).

While loan impairments in the US quickly skyrocketed from around one percent in 2007 to above five percent in 2009, Australia’s impairments remained steady at well under one percent. This can be seen in the chart below.

The adage of ‘you pay your mortgage before everything else’ is as true today as it ever has been in Australia.

Why Australian mortgages performed better than US mortgages during the GFC

The main reason Australian mortgages performed better than US mortgages during the GFC was due to the prudent underwriting standards employed by Australian banks and non-bank lenders.

To highlight the different standards, the best example is comparing US ‘sub-prime’ loans with its Australian equivalent, the ‘non-conforming’ mortgage. Unlike their US counterparts, Australian lenders:

- had lower average loan to value ratios

- did not offer introductory ‘teaser rates’ or high-risk repayment options, such as negative amortisation periods

- had ‘skin in the game’ via the lowest-rated tranche in a securitisation – this meant they were the first to lose capital in the event of any losses.

These factors culminated in investors in Australian structured credit holding higher quality underlying collateral than their US counterparts.

Structured credit 101

Structured credit investments are created through securitisation. This involves grouping similar loans and debt obligations such as mortgages, packaging them into interest-bearing securities backed by those assets and selling the cashflows to investors.

Structured credit issuers are predominately bank and non-bank financial institutions who undertake securitisation for a range of reasons, including lowering their financing costs through financing assets off balance sheet.

Securitisation plays an important role in the broader Australian economy as it increases competition amongst lenders and improves the flow of credit to consumers and businesses.

The opportunity for a higher yield, without higher incremental risk

Risk and return are often viewed as having a linear relationship. Securitisation can however offer investors an opportunity to earn a higher yield without incurring incremental risk. This is underpinned by the unique interplay between protection against loss, preferential yield characteristics and diversification.

Protection against loss

Each element of securitisation, from the transaction mechanics, collateral pool and loan servicer’s capability plays a critical role in protecting against loss. This multi-faceted design results in a highly defensive and resilient investment vehicle. This is evidenced by the fact investors in prime and non-conforming rated Australian RMBS transactions have historically experienced no loss of capital.1

Yield premium

Structured credit provides a yield premium compared to other similarly rated debt instruments. The premium reflects complexity rather than credit risk, as each element of securitisation requires detailed analytical risk assessment – across the structure, the servicer and the collateral. The increased level of diligence creates barriers to entry, limiting the universe of potential participants, effectively lowering supply and increasing yield.

Diversification

Structured credit benefits from a high degree of diversification, both in the underlying borrower collateral pool and type of asset. In a conventional loan, investors are exposed to a single borrower or asset, whereas in structured credit the investor’s risk is dispersed across thousands of underlying borrowers at smaller loan sizes.

The ‘Lifeblood of the business’

Securitisation is the lifeblood of many banks and non-bank financial institutions. These are ‘spread’ businesses, meaning they earn the difference between the rate at which they borrow funds and the rate at which they lend funds. This creates alignment between issuers and investors, as without funding they are unable to continue their core business – lending money.

Structured credit in the current environment

A carefully managed structured credit portfolio can provide investors with a unique opportunity to earn outsized risk adjusted returns. In addition to its attractiveness as a standalone investment strategy, structured credit also offers portfolio diversification for fixed income investors.

In the current environment characterised by persisting economic uncertainty and where the proliferation of corporate credit products has compressed yield, structured credit can be an attractive alternative.

As always, for investors, being able to identify (or selecting a manager able to identify) the right opportunities is key.

Please get in touch to arrange a discussion, and to learn more about our structured credit capabilities.

1 S&P

Important Information: This material has been prepared by MA Investment Management Pty Ltd (ACN 621 552 896) (“MA Financial Group”), a Corporate Authorised Representative of MA Asset Management Ltd (ACN 142 008 535) (AFSL 327 515). The material is for general information purposes and must not be construed as investment advice. This material does not constitute an offer or inducement to engage in an investment activity nor does it form part of any offer or invitation to purchase, sell or subscribe for in interests in any type of investment product or service. This material does not take into account your investment objectives, financial situation or particular needs. You should read and consider any relevant offer documentation applicable to any investment product or service and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision. This material and the information contained within it may not be reproduced or disclosed, in whole or in part, without the prior written consent of MA Financial Group. Any trademarks, logos, and service marks contained herein may be the registered and unregistered trademarks of their respective owners.

Nothing contained herein should be construed as granting by implication, or otherwise, any licence or right to use any trademark displayed without the written permission of the owner. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs of MA Financial Group. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. Additionally, this material may contain “forward-looking statements”. Actual events or results or the actual performance of a MA Financial Group financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. Certain economic, market or company information contained herein has been obtained from published sources prepared by third parties. While such sources are believed to be reliable, neither MA Financial Group or any of its respective officers or employees assumes any responsibility for the accuracy or completeness of such information. No person, including MA Financial Group, has any responsibility to update any of the information provided in this material.